In my attempt to learn in-depth the working style of prominent investors, I explored Ralph Wanger in my first such post. His book was amazing and gave a lot of insights.

This is my attempt to explore another great investor: Julian Robertson ( popularly called the ‘Tiger’). I recently read a lot about him, including a book on him, “The tiger in the land of the bulls”. The book was not so great but a good one time read nonetheless.

A Unique Zoo

In his famous talk, “The Superinvestors of Graham and Doddsville”, Buffett gave an analogy of a national coin flipping contest and says that if from the final winning population of 215 orangutans, 40 came from a specific zoo in Omaha, it warrants further investigation as to what is the reason for such concentration of success.

He was obviously referring to people who have taken the tenets of Value Investing as mentioned in the bible of investing, Security Analysis and applied those tenets in personal life.

Well, there are many such unique zoos. Obviously, the Graham & Doddsville is one of them but there are few more. One comes from a unique experiment and the inhabitants of this particular zoo are called ‘Turtle Traders’. Its a fascinating story which I will certainly cover sometime later but today I want to discuss another such Zoo and that is where the ‘Tiger’ resides along with his ‘Cubs’.

Tiger and the ‘Cubs’

Julian’Tiger’ Robertson came into the hedge fund industry after a discussion with the originator of the concept of hedge funds, A.W. Jones and formed his first hedge fund on the same model. But that is where the similarities end. The returns were nowhere close to other such hedge funds.

The returns he has generated are simply phenomenal. Let’s look things in more detail today.

Active Years

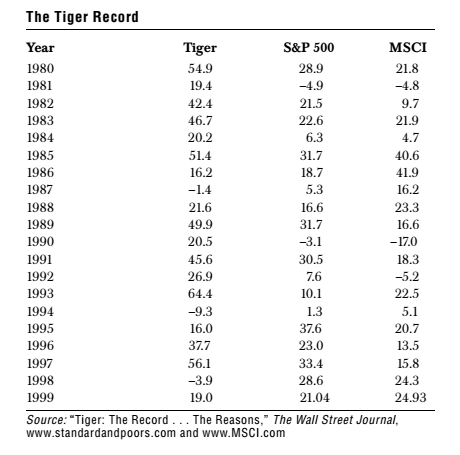

Tiger was active for the around 20 years. But here is the part that one should appreciate. He started his fund when he was 48 years old ( Inspiration for all those young turks who think they are late 😛 ) and his record is phenomenal. Have a look at the returns he generated

Well, that’s something.. Isn’t it ??

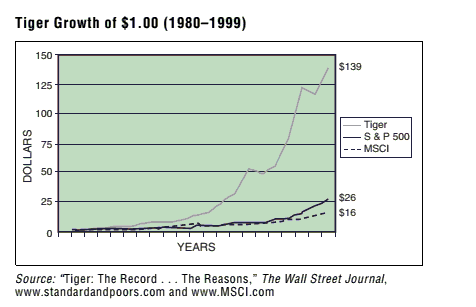

Here is another graphical way to appreciate his performance. Look at the equity curve shown below.

Style of Investing

Long and Short positions.

Even though his gamut of markets changed throughout the course of his career, he has always believed in taking both side positions and even though he wasn’t market neutral, the long and short style of investing does provided him a considerable amount of protection when the market direction goes South. I have discussed more in about this in Investment philosophy Section.

Markets of Tiger’s (and Cub’s) Interest

The markets where Tiger was active has been more of an outcome of his evolution. When he started, his area of interest was US equity markets and he would go long on the best ideas and short on the worst companies he could find. Later on, once the Tiger fund became big, he expanded his hunting ground to global markets and went beyond equities and played in commodities a lot.

Infact, the trade that really put him on the map was a trade in commodities only.

But for all the people looking for inspiration, be sure, that he didn’t do it because he was comfortable with it, but he was too big and wanted a bigger playing field. Infact, he , on many occasions, mentioned that he was primarily a stock picker.

Tiger’s “Breaking the Bank of England” Trade

Julian Robertson was ‘Big’ on Wall Street. But he wanted to be ‘Bigger’, an icon really..Some one as big as ‘George Soros’ was in the financial world. But what he lacked was not the skill or the knowledge but absence of ‘THE’ trade. The trade like ‘The Sterling trade’ of Soros, that made him ‘break the bank of England’ and become the icon that he was.

That trade came from the commodity markets. The trade was in Copper when he shorted the Copper as he was convinced that rise of the Copper prices was not warranted by an appropriate Supply Demand equation. He shorted and stuck to the position, despite the position being a losing one for long time. Well, if you are wondering how bad it was till the jackpot bell, the copper trade squeezed even Stan Druckenmiller out of his Copper shorts. In case you are not aware who Stan Druckenmiller is, he was the man holding and firing all the weapons for George Soros in the battle of Sterling.

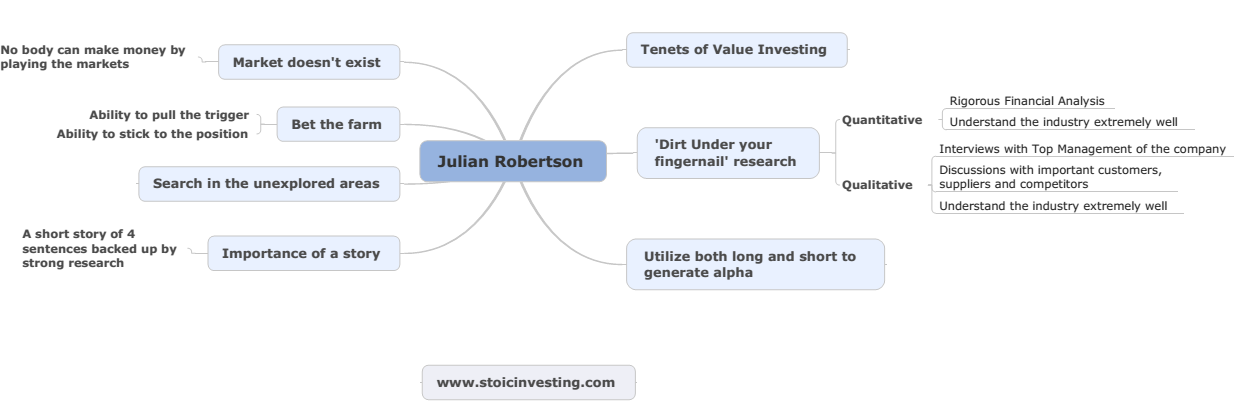

Investment Philosophy

Julian Robertson is a firm believer in the tenets of Value investing as mentioned by Graham in Security Analysis. From whatever I read, there are few key points of his investment philosophy which I zeroed down to.

Belief in the tenets of Value Investing

Find cheap companies which has the potential of value realization and invest in them and wait for them to give returns. Julian took the same argument to the other side too. He used to find expensive companies with high chance of value destruction and short them too. This is the next key point I want to discuss

Utilize both long and short to generate alpha

He was a firm believer in shorting and according to him, it expands his area of hunting, provided him with natural hedge against market direction and hence increase his alpha and decrease the draw-downs. His idea as explained by him was this:

“I believe that the best way to manage money is to go long and short stocks. My theory is that if the 50 best stocks you can come up with don’t outperform the 50 worst stocks you can come up with, you should be in another business.”

Shorting is a very different ball game than investing in long positions. In shorting, it’s not enough to have only valuation as the basis of shorting a company. A good company can (and most often will) stay over-valued for a long period of time. Hence it is important to bet against fundamentally flawed overvalued companies. Here is what Julian has to say about his short positions,

“For my shorts, I look for a bad management team, and a wildly overvalued company in an industry that is declining or misunderstood.”

In my conversation with Wesley Gray, I discussed the same points in detail.

One of my favorite investor and short seller, James Chanos said the same.He tries not to short on valuation but on “businesses where something is going wrong.” Some of his best ideas have been those that looked cheap but had “ensnared a lot of value investors.”

Search in unexplored territory

Tiger, like many other investors, including Ralph Wanger whom I discussed previously, had the fascination to look for opportunities in areas that are not well explored and hence he was fond of small cap companies. But this became difficult for him as the size of portfolio increased which made him expand his hunting ground rather than fighting in large caps where the advantage might not be that great. He gave an analogy of baseball to explain this.

“It is easier to create the batting average in a lower league rather than the major league because the pitching is not as good down there. That is consistently true; it is easier for a hedge fund to go to areas where there is less competition.”

‘Dirt under your fingernail’ research

The importance of extensive research was paramount for the Tiger and the analysts are the Tiger fund. They didn’t stop at just reading about stuff and doing extensive number crunching but go an extra mile to get a detail idea about the thesis they are working on. It was not about just ‘kicking’ the tires, It was more like ‘Dirt under your fingernail’ research.

The quantitative analysis was exhaustive with rigorous financial analysis. I am personally also a great fan of extremely exhaustive quantitative research on companies and industries that I am studying.

Qualitatively, Tiger made his analysts go beyond the industry reports and basic understanding of industries. The management meeting and the vision of the management was important for Julian Roberston. The analysts were supposed to get information from all other sources including the top customers, suppliers and competitors. That was the only way for them to be on the top of the industry where they were picking the companies.

Importance of the Story

For Julian, the presence of a story is very crucial in all investment ideas. The story (thesis) has to be simple, logical and grounded with thorough research. He always asked his analysts to zero down their months of research of an idea into easy, understandable 4 sentence idea. If the ideas sounds good, then and only then, he will move forward and then till the point the story doesn’t change, he would stick with the idea through thick and thin. That is very evident from his copper trade which went against him for a couple of years, which made even Stan Druckenmiller to close his position, but Julian remained with his position and that’s the reason he got a call from Stan to congratulate him on the trade.

Bet the farm

In the debate of how much money to put in a single idea, there was never an iota of doubt in Julian Robertson’s mind. If the story holds and the research is strong, the idea is to bet as big as possible. There are many times he has confirmed this. When some asked about his idea of investing, Robertson said,

“Smart idea, grounded on exhaustive research, followed by a big bet.”

I, personally, never understand why would anyone not bet big if the work done is good and the conviction is there. I see a lot of people, doing all the work on an idea and then investing insignificant amount. They saying things like, “It’s a 2% idea”. Whats the point ? Why invest 2% at all. You are better of looking elsewhere and find the next 10% idea than putting your money into partial conviction idea.

There is a second component to this whole idea. More often than not, the conviction of people in their ideas is not backed up by their commitment to the idea. That is what differentiate a great investor from a great analyst. There is nothing wrong in being a great analyst but when one is looking for inspiration for investing prowess, one has to understand the importance on the ability of pulling the trigger. Julian understands that and knows that its a great advantage he has. He said,

“There are not a whole lot of people equipped to pull the trigger.I’m normally the trigger-puller here.”

Market doesn’t exist

Julian Robertson have absolutely no belief in market timing. He is of a view that market doesn’t talk to anybody and he is not able to relate to people who say that they make money by timing the market. According to him, there is ‘No’ market. Its just a lot of companies listed and the prices action is individual and the only way to consistently make money is to buy companies at cheaper valuations and sell them when the valuations exceeds fundamental.

Cubs

Coming from the team of Julian Robertson, many analysts have later on started their own funds and are referred to as Cubs. Some of them have been backed by Julian Robertson himself. Some of them are legends in their own rights and hence I intend to cover them separately. The most popular ones are:

- John Griffin

- Chase Coleman

and many more…

I will write on them separately.

To write this, there are many resources, I have referred to. Here is the exhaustive list..

Resources

- Julian Robertson : A tiger in the land of the bulls and bear

- Money masters of our time

- More money than god

- Hedge Hunters

- Interview with Bloomberg

- Superinvestors of Graham and Doddsville

- Conversation with Wesley Gray